Keywords: Experiments, charitable contributions, methodology.

| (1) | (2) | (3) | (4) | (5) |

| Problem | Endowment | Condition | Hold | Pass |

| (for myself) | (to charity) | |||

| 1 | $8 | For every $1 you pass, the Charity will receive $1. | ||

| 2 | $8 | For every $1 you pass, the Charity will receive $2: your $1 and a matching $1 provided by the experimenter. | ||

| 3 | $8 | For every $1 you pass, the Charity will receive $1, and, the experimenter will refund to you $.50. |

| (1) | (2) | (3) | (4) | (5) |

| Problem | Maximum possible | Condition | Dollars in MPC | Dollars in MPC |

| contribution (MPC) | to pass to the | to hold for | ||

| charity | conversion to | |||

| your cash | ||||

| account | ||||

| 1 | $8 | No subsidy. Each $1 of the MPC represents $1 you donate to the charity from your cash account. Cash Account: $8 | ||

| 2 | $16 | 100% Matching Subsidy: Each $1 of the MPC consists of $.50 you donate from your cash account and a $.50 matching contribution provided by the experimenter. Cash Account: $8 | ||

| 3 | $16 | 50% Refund Subsidy. Each $1 of the MPC consists of $1 you donate from your cash account, but with $.50 of this donation refunded back to your cash account by the experimenter. Cash Account: $8 |

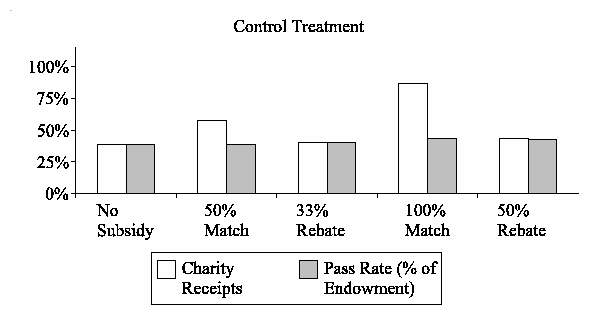

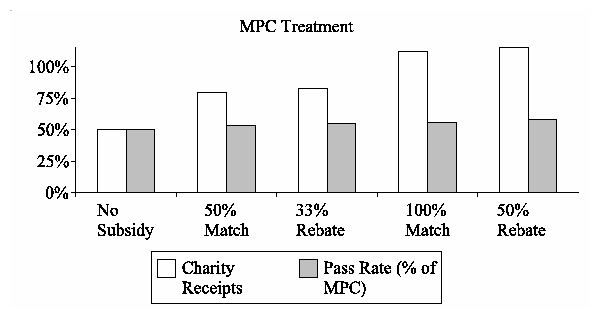

Results of the MPC treatment, shown in the bottom panel of Figure 1

suggest that switching the directly presented problem dimension from an

endowment to the maximum amount a charity may receive eliminates any

effect of matching subsidies on charity receipts. When people divide

charity receipts (the hollow bars), contributions move directly with

the effective price of contributions, regardless of whether a rebate

subsidy or a matching subsidy induced the price reduction. Notice

again that the pass rates in the MPC treatment remain roughly constant

at all endowment levels and effective prices of contributions.

The charity receipt and pass rate data presented in Tables 3 and 4 allow

a quantitative evaluation of the results suggested by Figure 1.

Consider first charity receipts expressed as a percentage of

endowments, shown in Table 3. In the table, the entries in column (3)

list charity receipts in the no subsidy condition, while entries in

columns (4) and (5) list charity receipts for comparable matching and

rebate subsidy conditions. For example, as indicated by the entry in

column (3) of row (a), given a $12 endowment mean charity receipts in

the no subsidy condition of the control treatment equaled 38% of

participants' endowments. Similarly, the entries in columns (4) and

(5) of row (a1) indicate that given an effective contributions price of

$0.67, and again a $12 endowment, mean charity receipts in the

control treatment were 53% of participants' endowments under the

(50%) matching subsidy, and 39% of participants" endowments in the

comparable (33%) rebate condition.

Results of the MPC treatment, shown in the bottom panel of Figure 1

suggest that switching the directly presented problem dimension from an

endowment to the maximum amount a charity may receive eliminates any

effect of matching subsidies on charity receipts. When people divide

charity receipts (the hollow bars), contributions move directly with

the effective price of contributions, regardless of whether a rebate

subsidy or a matching subsidy induced the price reduction. Notice

again that the pass rates in the MPC treatment remain roughly constant

at all endowment levels and effective prices of contributions.

The charity receipt and pass rate data presented in Tables 3 and 4 allow

a quantitative evaluation of the results suggested by Figure 1.

Consider first charity receipts expressed as a percentage of

endowments, shown in Table 3. In the table, the entries in column (3)

list charity receipts in the no subsidy condition, while entries in

columns (4) and (5) list charity receipts for comparable matching and

rebate subsidy conditions. For example, as indicated by the entry in

column (3) of row (a), given a $12 endowment mean charity receipts in

the no subsidy condition of the control treatment equaled 38% of

participants' endowments. Similarly, the entries in columns (4) and

(5) of row (a1) indicate that given an effective contributions price of

$0.67, and again a $12 endowment, mean charity receipts in the

control treatment were 53% of participants' endowments under the

(50%) matching subsidy, and 39% of participants" endowments in the

comparable (33%) rebate condition.

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

| Mean CR (s.d.) | t (matched pairs tests) | |||||||

| (lr)4-6 (lr)7-9 | Price of $1 | No | ||||||

| Endowment | contribution | subsidy | Match | Rebate | M v. NS | R v. NS | M v. R | |

| (a) | $12 | $1.00 | 0.38 | |||||

| (0.20) | ||||||||

| (b) | $8 | $1.00 | 0.39 | |||||

| (0.23) | ||||||||

| (a1) | $12 | $0.67 | 0.53 | 0.39 | 5.09 | 0.30 | 5.15 | |

| (0.30) | (0.23) | |||||||

| (a2) | $8 | $0.67 | 0.63 | 0.41 | 6.55 | 0.96 | 8.60 | |

| (0.31) | (0.23) | |||||||

| (b1) | $12 | $0.50 | 0.82 | 0.44 | 6.72 | 2.03 | 7.97 | |

| (0.46) | (0.23) | |||||||

| (b2) | $8 | $0.50 | 0.91 | 0.42 | 6.21 | 1.18 | 7.35 | |

| (0.57) | (0.19) | |||||||

| (c) | $12 | $1.00 | 0.49 | |||||

| (0.35) | ||||||||

| (d) | $8 | $1.00 | 0.49 | |||||

| (0.34) | ||||||||

| (c1) | $12 | $0.67 | 0.77 | 0.79 | 5.74 | 7.72 | -0.85 | |

| (0.46) | (0.46) | |||||||

| (c2) | $8 | $0.67 | 0.80 | 0.83 | 7.73 | 9.26 | -0.67 | |

| (0.47) | (0.45) | |||||||

| (d1) | $12 | $0.50 | 1.10 | 1.16 | 10.61 | 10.59 | -1.28 | |

| (0.60) | (0.57) | |||||||

| (d2) | $8 | $0.50 | 1.14 | 1.13 | 10.80 | 9.82 | -0.27 | |

| (0.56) | (0.62) | |||||||

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

| Mean CR (s.d.) | t (matched pairs tests) | |||||||

| (lr)4-6 (lr)7-9 | Price of $1 | No | ||||||

| Endowment | contribution | subsidy | Match | Rebate | M v. NS | R v. NS | M v. R | |

| (a) | $12 | $1.00 | 0.38 | |||||

| (0.20) | ||||||||

| (b) | $8 | $1.00 | 0.39 | |||||

| (0.23) | ||||||||

| (a1) | $12 | $0.67 | 0.35 | 0.39 | -1.67 | 0.29 | -1.99 | |

| (0.20) | (0.23) | |||||||

| (a2) | $8 | $0.67 | 0.46 | 0.42 | 1.91 | 0.96 | 0.28 | |

| (0.29) | (0.19) | |||||||

| (b1) | $12 | $0.50 | 0.41 | 0.44 | 0.73 | 2.03 | -0.87 | |

| (0.23) | (0.23) | |||||||

| (b2) | $8 | $0.50 | 0.42 | 0.41 | 1.50 | 1.18 | 0.86 | |

| (0.20) | (0.23) | |||||||

| (c) | $12 | $1.00 | 0.49 | |||||

| (0.35) | ||||||||

| (d) | $8 | $1.00 | 0.49 | |||||

| (0.34) | ||||||||

| (c1) | $12 | $0.67 | 0.50 | 0.53 | 0.31 | 1.14 | -1.08 | |

| (0.30) | (0.31) | |||||||

| (c2) | $8 | $0.67 | 0.53 | 0.56 | 1.31 | 2.51 | -0.83 | |

| (0.32) | (0.30) | |||||||

| (d1) | $12 | $0.50 | 0.55 | 0.58 | 1.49 | 2.19 | -1.48 | |

| (0.30) | (0.29) | |||||||

| (d2) | $8 | $0.50 | 0.56 | 0.56 | 1.86 | 1.93 | -0.03 | |

| (0.29) | (0.31) | |||||||