Previous research has demonstrated that consumers’ decisions

regarding supplementary pensions could be affected by biases.

Bernatzi and Thaler’s experiment demonstrated that menu design can

influence pension fund enrollment decisions, in that participants

appear to adopt a naïve heuristic, i.e., “extremeness aversion”.

Using a database of 27 occupational pension funds from 2007 to 2011,

representing 1,732,530 employees, this study asked whether menu

design affected Italian workers’ choices regarding the supplementary

pension system as a result of the new rules enacted by the regulator

in 2007. Most enrolled workers opted for the median investment

line. I discuss the possible relevance of this result to public

policy, in particular the possibility of including these preferences

in the regulations, with the aim of benefiting employees.

On 1 January 2007, the Italian government introduced an important and

wide-ranging reform of the pension system, designed primarily with

employees in mind, having the aim of increasing and developing the

supplementary pension scheme.1 The

reform, which was explained to employees by means of flyers and

announcements in the mainstream mass media, basically presented

workers with three alternatives to choose from, two explicit and one

tacit. The two possible expressed alternative options are:

a) to indicate the name of the pension fund the employee wants to

enroll with. This pension fund will collect the employee’s and the

employer’s contributions and accumulated severance pay;

b) to declare his/her willingness to leave accumulated severance pay

with the employing company and therefore decide not to enroll with any

pension fund. In this case, if the company has more than fifty

employees, the employer must switch the accumulated severance pay to

the “Treasury fund” held by the National Social Security Institute

(INPS).2

If the employee does not express any choice (so called

“tacit-members”), the tacit option works by providing automatic

enrollment with, and depositing of accumulated severance pay in, one

of the following alternative options:

1) the pension fund identified by collective agreement or by company agreement;

2) if point 1 does not apply, the pension fund that has the highest number of company employees;

3) if points 1 and 2 do not apply, the INPS Fund3, created and managed by

INPS.

Table 1: Number of Italian occupational pension funds related to

number of investment lines (2007-2011), drawn from the Covip Annual

Report (2007-2011) and Italian occupational pension funds’ balance

sheets (2007-2011)

Number of investment lines

2

3

4

5

Number of occupational pension fund plans examined

6

13

6

2

After choosing the pension fund in which to enroll, either

explicitly or tacitly, the worker is asked to choose one or more

investment lines4. Again, on the one hand, if the

employee decides not to decide (“tacit-member”), the

law5 identifies as the

default option the guaranteed line without any risk (no-risk

investment line). On the other hand, the members who make an explicit

choice (“explicit member”) decide which line to enroll in from those

available in each Italian occupational pension fund.

Past literature includes many studies by authors who have considered

how people made decisions in financial settings (Kahneman and Tversky,

1984; Kahneman and Knetsch, 1992; Levin et al., 2002; Kahneman, 2003)

and how people decide portfolio asset allocation, including that for

their supplementary pension. Bernatzi and Thaler (2002) in particular

found “extremeness aversion” in pension fund asset allocation

choices. Benartzi and Thaler found that menu design can influence

pension fund enrollment decisions. They asked UCLA plan participants

to select an investment from three different menus. The investment

lines offered ranged from A (low risk) to D (high risk). The first

menu included options A, B, and C; the second one, just options B and

C; the last one, options B, C, and D. Comparing options B and C, which

appeared in all three menus, 29% of participants preferred C over B

in the first menu; 39% in the second menu and 54% in the third

menu. This result shows that, in the first menu, where option C was an

extreme, it was the least popular; in the third menu, where option C

was the middle choice, it was the most popular. Thus Benartzi and

Thaler’s (2001) experiment demonstrates that participants appear to

use a naïve heuristic (i.e., “avoid extremeness”) rather than

maintaining a consistent set of well-ordered risk preferences. Bearing

in mind these results, the present paper aims to test whether the

explicit members in Italian occupational pension funds asset

allocation choices have been influenced by the menu design in order to

identify a middle option predominance.

The results presented in this paper expand the existing literature on

the topic of pension fund enrollment decisions considering a new

unexplored market, Italy, and at the same time, they could be taken

into consideration by the regulators, with the aim of benefiting

employees.

The paper is organized as follows: Section 2 presents the sample;

Section 3 presents the methodology and the results; Section 4 comments

on the main results obtained and concludes.

2 Data sample

The sample used in this paper was created from the list of

occupational pension funds identified and recognized by the Pension

Funds Supervision Commission (COVIP) (a total of 35) at the end of

2007, the year of the introduction of Italian pension reform . Those

no longer operating at the end of 20116 (two) were eliminated. The occupational pension funds

existing before 2007 which did not provide a guaranteed investment

line had to introduce one in order to be able to enroll the tacit

members, as provided for by law.7 For

this reason 2007 represents a year of strong discontinuity with the

past.

For each occupational pension fund, we analyzed the balance sheets

from the years 2007–2011 in order to gather information about: a) the

number and the types of investment lines offered in each fund; b) the

total number of subscribers at the end of each year examined; c) the

number of new subscribers enrolled during each year; d) the total

number of tacit members at the end of each year examined; and e) the

number of new tacit members enrolled during each year

examined. Therefore the occupational pension fund whose balance sheets

did not show the distinction between tacit and explicit members as

well as the total number of tacit members at year-end or the number of

tacit members acquired during the years examined were

eliminated. After this selection, of the original 33 Italian

occupational pension funds representing 1,988,639 members, our final

sample comprised 27 occupational pension funds (that is to say

81.82%), representing 1,732,530 members (87.12%) at the end of

2007. In order to assess the presence of predominant behavior in

Italian occupational pension fund asset allocation choices, only

expressed choices can be considered, given that the tacit members do

not express any choice but simply accept the default option determined

by law. For this reason, the total number of guaranteed-line members

was reduced by the number of tacit members. In addition, we consider

the Italian occupational pension funds based on the number of

investment lines offered by each one, as shown in Table 1.

In each occupational pension fund, investment lines are presented to

workers sorted by the level of risk, from no-risk (also called

“guaranteed line”) to higher risk, with increasing order. In fact,

according to the Pension Funds Supervision Commission (COVIP)

guidelines, the guaranteed line is the investment line without any

risk, so the expected loss by members is zero; the “very low risk

line” is the investment line for which the expected annual loss by

its members is maximum 10%; the “low risk line” considers the

possibility of maximum 30% expected loss per year; “balanced” is

the investment line for which the expected loss by its members is

(maximum) from 30% and 50%; “growth” is the investment line for

which the expected loss could be even higher than 50% per

year.8

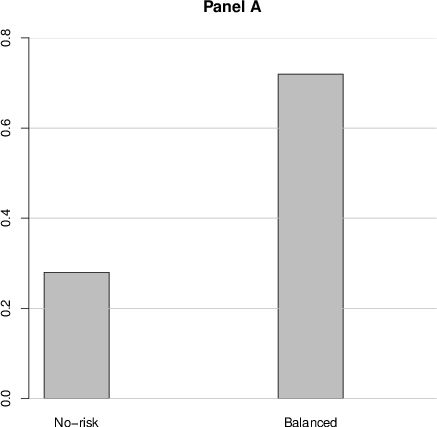

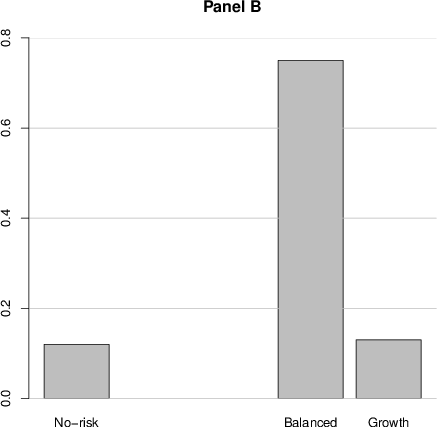

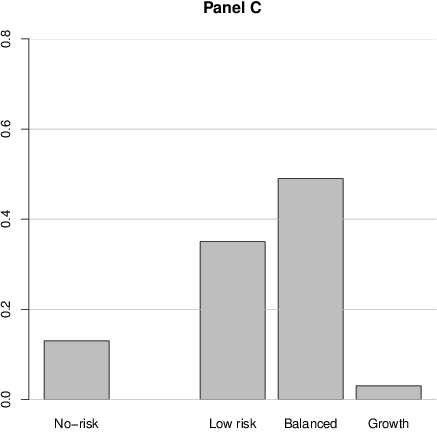

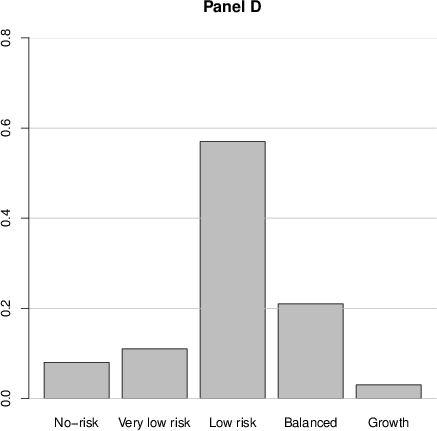

Figure 1: Subscribers distribution of the Italian occupational

pension funds investment line at year-end 2007–2011, elaborated by

the author based on the number of explicit members enrolled in

each investment line per Italian occupational pension fund

(year-end 2007-2011).

3 Methodology

The methodology used in this paper comprises two steps: Step 1

is designed to show the graphic evidence of the subscribers

distribution in investment line choices made by explicit members in

Italian occupational pension funds from 2007 to 2011; Step2

involves the econometric analysis of the graphic evidence identified

in Step1.

3.1 Step 1

Each Italian occupational pension fund is reserved for a defined

category of workers; if new workers join this category they can also

join the pension fund. In 2007, Italian workers were asked to choose

between the two, three, four and five investment lines respectively

offered by their occupational pension fund. Graph 1 shows subscriber

distribution over investment lines and years (2007–2011) for Italian

occupational pension fund enrollment. Initial consideration of panels

B, C, and D reveals graphic evidence of a strong middle option

predominance in Italian occupational pension fund asset allocation

choices.

Table 2: The middle choice predominance in Italian occupational pension funds

calculated by the HHI, calculated on the basis of the number

of subscribed members (year-end 2007-2011) taken from the balance

sheet of each Italian occupational pension fund.

Investment lines:

2

3

4

5

No-risk

805.93

134.47

169.15

36.44

Very low risk

117.84

Low risk

1218.32^*

2735.13^**

Medium risk

5128.14^**

5691.39^**

2378.31^**

695.17

High risk

168.02

11.03

19.74

Notes: * indicates medium concentration; ** indicates high concentration.

However, on the one hand, faced with an even number of choices menu,

panels A and C, in which there is a non-dominant choice, employees

tend to opt for an intermediate or compromise alternative (Tversky &

Simonson, 1993). In panel A only two alternative options are available

so a middle choice is not identifiable. In general, in a binary choice

polarization could occur (Chernev, 2004). In fact, as shown in panel

A, the medium risk alternative tends to attract most employees’

choices. However, in panel C there are two middle choices, not only

one; in this case employees tend to choose this two middle

alternatives. On the other hand, faced with an odd number of choices

menu, panels B and D, there is a strong middle choice predominance.

The graphic evidence is also confirmed by statistical analysis. In

particular, choice of the Balanced fund is significantly greater when

it is the middle option, in Panel B, than when it is one of two

options, in Panel A, for each of the 5 years, despite the fact that

some of those who choose the Balance fund in Panel A would have chosen

the Growth fund in B. Overall the difference was 75.8% vs. 71.4%,

again a small difference, but enough to be significant every year by a

χ2 test at p<10−10, because of the large number of

members.

Choice of the Low-risk fund was much greater when it was the middle

option, in Panel D (67.0% overall) than when it was not, in Panel C

(34.9%). Again this difference was highly significant in each of the

5 years. Preference for the middle option might be especially strong

when members have more options to choose from.

3.2 Step 2

Table 3: Description of variables, for data collected from each

Italian occupational pension fund’s balance sheet (year end

2007-2011).

Variable

Description

Dependent variable:

type

Investment line type, from 0 to 4. The investment

line risk increases from the guaranteed line (0)

to very high risk (4).

Independent variables:

sub

Total number explicit members at year end

sub2

Total number explicit members squared at year end

performance

Yearly performance for each line

t1, t2, t3, t4, t5

Time dummies (t1=2007; t2=2008; t3=2009; t4=2010; t5=2011)

Note: Other independent variables—such as:

the Total Expensive Ratio (TER) per investment line obtained from the

Covip web site; and the worker macro-categories obtained according to each Italian

occupational pension fund’s status—were included in the analysis,

but these variables (individually or included together) did not give

any results. For this reason they were eliminated.

To test in another way the appeal of the middle choice in Italian

occupational pension fund asset allocation choices, the Herfindahl

Hirschman Index (HHI)9 was calculated using the following equation:

HHI =

n

∑

i=0

(100 si)2

(1)

Table 4: Panel regression analysis of extremeness aversion(2007-2011)

In Equation 1, si, is the single investment line proportion per

different menu design, i is the investment line type from 0

(guaranteed line—no risk) to 4 (very high risk investment

line—growth). The use of HHI is the most appropriate. In fact each

Italian occupational pension fund is reserved for a defined category

of workers (if new workers join this category they can also join the

pension fund) representing its potential market; the investment line

opportunities offered in each fund are therefore in competition with

each other and they are presented to workers in order of increasing

risk; if the middle investment line/s is more attractive, a

predominance for the central choice is identifiable. The HHI results,

shown in Table 2, indicate a strong concentration in the middle

investment line/s in each occupational pension fund, except for the

two investment lines in which there is “polarization”.

The middle investment line is generally the most popular; this

situation is anomalous and can be explained by factors including the

influence of menu design on decision making and the inconsistent set

of well-ordered risk preferences (Simonson, 1989).

To test the existence of the middle option predominance, so as to

confirm the HHI results, an ordered logistic regression

(OLOGIT)10 is used as follows:

type = α sub + β sub2 + γ

performance +

d1t1 + d2t2 + d3t3 + d4t4 + d5t5 + ε

(2)

The dependent variable “type” assumes values from 0 to 4 according

to the investment line risk level. The OLOGIT model is justified to

test the presence of the predominant central investment line choice

bearing in mind that the menu design presents the investment lines

with a specific increasing risk level order. The variables used in the

model are shown and described in Table 3.

Considering the two-investment-line choice, the meaning of the

sub-squared coefficient indicates a growing trend of hyperbole to

confirm the polarization phenomenon. With reference to the other lines

(3, 4 and 5) the sub-squared coefficient is negative and statistically

significant, and the sub coefficient is positive and statistically

significant; this identifies a parabola with a peak, with the

confirmation of the concentration of explicit members’ choices in the

middle. Table 4 shows that investment line performance is not

statistically significant, that is to say that subscribers’ choices

are not influenced by it. This factor is important because it leads us

to the conclusion that the impact of investment menu design on

participant investment choices in Italian occupational pension funds

has a more powerful influence on the decision-making process than the

underlying risk and performance characteristics of the investment

lines offered (Benartzi and Thaler, 2002; Agnew and Szykman, 2005).

4 Conclusions

Bearing in mind the wide gap between the moment in which the choice is

made and the future time of “enjoyment”, a wrong or unsuitable asset

allocation choice in terms of pension funds could seriously compromise

the maintenance of living standards after retirement. The results

presented here show that many Italian occupational pension fund

subscribers opt for the middle option. Choices influenced by menu

design could often be contrary to rationality, not being dictated by

an awareness of risk profiles. In this context, the dilemma arises as

to which would be the optimal number of investment lines to make

available in occupational pension funds. A solution could be the

introduction of a life-cycle investment line, independently followed

by a manager who would change asset allocation depending on the

member’s age. The regulator could adopt this kind of investment line

for tacit members; at the same time it could consider standardizing

the number of investment lines in each occupational pension fund, for

example, five, the life-cycle line being in the middle. Further

research in this area could be a source of inspiration for Italian

(and other) regulators, exploiting these specific middle-favoring

biases to the subscribers’ benefit.

References

Agnew, J., & Szykman, L. (2005). Asset allocation and information overload: the

influence of information display, asset choice, and investor experience,

Journal of behavioral finance, 6, 57–70.

Benartzi, S., & Thaler, R. (2001). Naïve diversification strategies in defined

contribution saving plans, American Economic Review, 91, March,

79–98.

Benartzi, S., & Thaler, R. (2002) How much is investor autonomy worth?,

Journal of finance, 57, August, 1593–1616.

Chernev, A. (2004). Extremeness aversion and attribute-balance effects in

choice, Journal of consumer research, 31, 249–263.

Festinger, L. (1957). A theory of cognitive dissonance, Stanford C.A.:

Stanford University Press.

Gourville, J., & Soman, D. (2007). Extremeness seeking: when and why

consumers prefer the extremeness, HBS-working paper n. 07–092, May.

Kahneman, D. (2000a). A psychological point of view: violations of rational

rules as a diagnostic of mental processes, (Commentary on Stanovich and West),

Behavioral and brain science, 23, October, 681–683.

Kahneman, D. (2000b). Experienced utility and objective happiness: A

moment-based approach. In D. Kahneman and A. Tversky, Choice, values,

and frames. New York: Cambridge University Press.

Kahneman, D. (2003). Maps of bounded rationality: psychology for behavioral

economics. The American economic review, 93, 1449–1475.

Kahneman, D., & Knetsch, J. (1992).Valuing public goods. The purchase of moral

satisfaction, Journal of environmental economics and management,

57–70.

Kahneman, D., & Tversky, A. (1979). Prospect theory: an analysis of decision

under risk. Econometrica, 263–291.

Kahneman, D., & Tversky, A. (1994). Choices, values and frames, American

psychologist(39).

Kahneman, D., Knetsch, J., & Thaler, R. (1991). The endowment effect, loss

aversion, and status quo bias, Journal of economic perspectives, 5

, 193–206.

Levin, P., Gaeth, G., & Schreiber, J. (2002). A new look at framing effects:

distribution of effect sizes, individual differences, and independence of types

of effects, Organizational Behavior and Human Decision Processes,

88, 411–429.

Simonson, I. (1989). Choice based on reasons: the case of attraction and

compromise effects, Journal of consumer research, 16,

158–174.

Tversky, A., & Kahneman, D. (1981). The framing of decisions and the psychology

of choice, Science (211).

Tversky, A., & Kahneman, D. (1992). Advances in prospect theory. Cumulative

representation under uncertainty, Journal of risk and uncertainty, 5,

297–323.

Tversky, A., & Simonson, I. (1993). Context-dependent preferences,

Management science, 39, 1179–1189.

Department of Business Administration,

Faculty of Economics, Università Cattolica del Sacro Cuore

(Piacenza Site), Italy, Via Emilia Parmense 84, 29122 Piacenza

(Italy). Email: andrea.lippi@unicatt.it.

All pension fund statutes establish the

number and the types of lines in which the workers can

invest. Moreover, the statute stipulates whether it is possible to

diversify across lines or not.

In panel D, workers were removed not only when their

assignment was tacit according to government rules but also when

they were assigned to new lines as the result of a merger of two

companies. Many of these workers were assigned to the low-risk and

growth lines, which would have higher numbers if they were

included.

The HHI is designed to measure industry

concentration. The US Department of Justice associates the following

threshold values with the HHI for particular use: an HHI below 1,000

signals a low concentration, while one above 1,800 signals a high

concentration; an index between 1,000 and 1,800 shows a moderate

concentration.

Ologit fits ordered logit models of ordinal variable

on the independent variables. For example, to test if “health”

(0=bad; 1= not so good; 2=good; 3=very good) is depending by gender,

skin color and/or age an ologit regression can be used as follows:

ologit health female black white age.