| Figure 1: Punishment recommendations in days of community service as a function of whether the victim was insured, uninsured, or insurance not mentioned (Experiment 1). Error bars represent ±1 standard error. |

Judgment and Decision Making, vol. 8, no. 2, March 2013, pp. 161-173

The insured victim effect: When and why compensating harm decreases punishment recommendationsPhilippe P. F. M. van de Calseyde* Gideon Keren# Marcel Zeelenberg# |

An insurance policy may not only affect the consequences for victims but also for perpetrators. In six experiments we find that people recommend milder punishments for perpetrators when the victim was insured, although people believe that a sentence should not depend on the victim’s insurance status. The robustness of this effect is demonstrated by showing that recommendations can even be more lenient for crimes that are in fact more serious but in which the victim was insured. Moreover, even when harm was possible but did not materialize, people still prefer to punish crimes less severely when the (potential) victim was insured. The final two experiments suggest that the effect is associated with a change in (1) compassion for the victim and (2) perceived severity of the transgression. Implications of this phenomenon are briefly discussed.

Keywords: insured victim effect, punishment, insurance, interpersonal judgment.

The costly consequences of negative events may be compensated for by insurances. As such, an insurance policy lowers the risk of the insured. However, research has shown that controlling risk via insurances also comes at a cost. For example, when buying insurance, people tend to make decisions that are incompatible with rational choice theory (e.g., Johnson, Hershey, Meszaros, & Kunreuther, 1993). In this article, we address a very different potential cost of insurance, namely, whether people would recommend lower punishments for crimes in which the victim was insured as opposed to uninsured. Interest in this issue stems from the fact that compensating harm may change the victim’s outcome, yet it does not alter the severity of the crime. It often implies only a transfer of the negative consequences from the victim to the insurance company. When victim compensation from insurance indeed improves the perpetrator’s outcome, the insurance policy may prove to be a safeguard for the perpetrator as well.

In essence, an insurance policy is a safety mechanism by which a third party (the insurance company) undertakes to guarantee an insured party against losses that may be incurred by misfortunes. Insurance thus changes the severity of an unfortunate outcome by providing financial compensation in the event that a specific hazard occurs. A large stream of literature in both economics and psychology has focused on understanding the consequences of insurance from the perspective of the insured party (e.g., Holmstrom, 1979; Tykocinski, 2008; Hsee & Kunreuther, 2000; Johnson et al., 1993). For example, one of the unwanted side effects of insurance is the phenomenon of moral hazard. It refers to the increased risk taking by individuals for whom the consequences of risk are reduced which, in turn, increases the probability that misfortune will strike. Research revealed a positive correlation between accidents and car insurance benefits and a positive correlation between health insurance and unhealthy lifestyles (e.g., Stanciole, 2007; Dave & Kaestner, 2009). In addition, Tykocinski (2008) found that reminding people of their insurance policy lowered their perceived likelihood that misfortune will befall them (but see Van Wolferen, Inbar & Zeelenberg, 2013). Together, these findings suggest that being insured may create an illusory sense of safety resulting in detrimental behavioral consequences.

We build upon this prior work and extend it in order to understand the interpersonal consequences of insurance. Specifically, we investigate whether people would recommend different punishments for crimes in which the victim was insured as opposed to uninsured. To illustrate our point, imagine two thieves both of whom stole an identical digital camera from two different people. One of the victims happened to be insured against theft while the other was not. Two related questions can be raised concerning the punishment the thieves deserve: (1) should they be punished equally (the normative question) and (2) will they be punished equally (the descriptive question)? Building on prior work on how the outcome of victims may influence sentencing decisions (e.g., Gino, Shu, & Bazerman, 2010; Gino, Moore, & Bazerman, 2009; Berg-Cross, 1975), we find that (1) although people believe that sentencing should not depend on whether a victim was insured or not, (2) people nonetheless recommend lower punishments for perpetrators when the victim was insured as opposed to uninsured.

Harm and punishment are intimately related. When a person is unjustly harmed, people experience a strong desire to punish the wrongdoer (Carlsmith, Darley, & Robinson, 2002) and more harm is typically accompanied with more punishment. In fact, legal systems are often rooted in the premise that punishments should be proportional to the harm caused (e.g., an eye for an eye) and there is widespread consensus that this “just deserts” principle is a justified moral rule (Carlsmith et al., 2002). However, using the severity of harm as a guide may also prompt people to use the victim’s outcome in a manner that can sometimes be normatively irrelevant (Gino et al., 2009, 2010; Paharia, Kassam, Greene, & Bazerman, 2009; McCaffery, Kahneman, & Spitzer, 1995; Berg-Cross, 1975). For example, research by Cushman, Dreber, Wang, and Costa (2009) indicates that people punish behaviors that accidentally resulted in small detrimental consequences less harsh as compared to similar acts that by accident resulted in large consequences. In a similar vein, multiple studies by Gino and colleagues (2010) reveal that people are less likely to punish unfair behaviors when the unfairness happened to produce positive rather than negative consequences for a victim. Together, these studies suggest that people use the severity of a victim’s outcome as a guide in evaluating and sentencing perpetrators. Since insurance positively changes the severity of the consequences for a victim, we hypothesized that, other things being equal, people will recommend lower punishments for crimes in which the victim was insured as opposed to uninsured.

Six experiments were conducted to examine this effect. Experiment 1 provides initial support for the hypothesized relationship between the extent to which a victim is insured or not and the corresponding severity of punishment. Experiment 2 aims to determine whether people knowingly punish perpetrators less severely when victims are insured, by asking participants to judge both the insured and uninsured conditions simultaneously. Experiment 3 extends these findings by looking at the role of foreknowledge of the perpetrator. Experiment 4 tests whether people would also differentiate between insured and uninsured individuals when punishing a transgression that did not result in any harm. Experiment 5 aims to determine whether people would also punish perpetrators more mildly when the crime against the insured victim was in fact more severe. Finally, Experiment 6 examines the role of possible psychological processes that may explain why people are more lenient towards perpetrators when the victim happened to be insured.

Participants. Twenty-nine students (6 male, 23 female) at Tilburg University participated in exchange for course credit (Mage = 19, SD = 1.40).

Design and procedure. All participants were asked to read a brief scenario concerning a theft of a camera and subsequently were asked to determine the severity of punishment the thief deserved. Participants were randomly assigned to the insurance or no insurance condition. The scenario in the insurance [no insurance] condition read as follows:

Tom is an amateur photographer who decides to purchase a new camera. In the store he is asked if he wants to insure the camera against theft. This type of insurance guarantees that Tom will receive a new camera in case the camera is stolen.Although Tom doubts whether to buy the insurance, he decides [not] to do so. In short, his camera is [not] insured against theft. A few days later when Tom is sitting on the terrace in the city and wants to leave, he discovers that his camera is stolen.

Some time later Tom finds out that a person was arrested who confessed stealing and selling the camera. A common punishment for such an offence is imposing community service. Community service entails doing compulsory social work for several days (8 hours a day).

After reading the scenario, participants were asked to make a punishment recommendation by indicating the number of days (minimum 1 day, maximum of 20 days) they thought the perpetrator should fulfill community service.

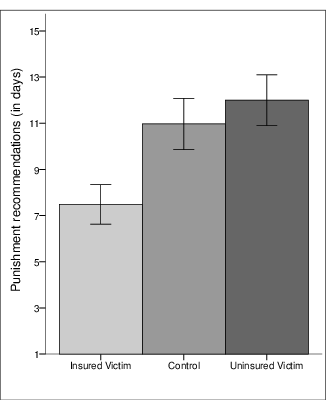

Figure 1: Punishment recommendations in days of community service as a function of whether the victim was insured, uninsured, or insurance not mentioned (Experiment 1). Error bars represent ±1 standard error.

Participants recommended less severe punishments when the camera was insured (M = 9.20; SD = 5.98) as compared to when it was uninsured (M = 13.93; SD = 5.42), t (27) = 2.23, p = .04, d = 0.83. These findings confirm the initial prediction that people would punish the same transgression differently as a function of whether the victim was insured or not. These results can be interpreted in two ways. One possibility is that people recommend more severe punishments when stealing an uninsured possession. Alternatively, it may be the case that people recommend a milder punishment when the victim was insured. An additional study was designed to addresses this issue by including a baseline condition in the experimental design.

Additional study. Besides replicating the previous results, the purpose of this experiment was to test whether the uninsured condition would be punished more severely than a neutral baseline or whether the insured condition would be punished less severely than the same baseline. The procedure, scenario and dependent measure were identical as the one used in the previous experiment except that a baseline condition was added which did not mention the possibility of buying insurance. Ninety-nine individuals at various locations in Tilburg (46 male, 53 female) volunteered to participate in this study (Mage = 25, SD = 8.44). Punishment recommendations again varied as a function of insurance, F (2, 96) = 5.30, p = .007, η ² = .11 (Figure 1) thus replicating the results of the first experiment. Planned comparisons showed that participants again imposed milder punishments on a perpetrator who stole an insured camera (M = 7.48; SD = 4.93) compared to a perpetrator who stole an uninsured camera (M = 12.00; SD = 6.30), p = .002, d = 0.80. Likewise, participants recommended a milder punishment on a perpetrator who stole an insured camera as compared to baseline participants (M = 10.97; SD = 6.37), p = .02, d = 0.61. Punishment recommendations did not vary between the uninsured and the baseline condition (t < 1, ns.). This pattern shows that, compared to the neutral baseline, people recommend milder punishments when victims are insured and not harsher punishments when victims are uninsured.

The above results demonstrate that people differentiate between insured and uninsured victims when judging both cases separately. Would people still differentiate between both victims when evaluating the two cases jointly? Joint evaluations allow decision makers to comparatively evaluate multiple options while in separate evaluation only one of two options is evaluated. Previous research demonstrated preference reversals between what people choose in separate versus joint evaluation (Hsee, 1996; Hsee & Zhang, 2010). Joint-separate evaluation reversals demonstrate that switching from one evaluation mode to the other changes the relative importance that people assign to a given attribute (in our case, stealing an insured versus uninsured possession). Importantly, joint evaluations allow us to determine whether people believe they should differentiate between insured and uninsured victims when sentencing perpetrators (for similar reasoning, see Bazerman, Tenbrunsel, & Wade-Benzoni, 1998). The present experiment therefore manipulated evaluation mode by asking participants to assess the appropriate punishment for the theft of an insured as well as an uninsured camera. The purpose of this design was to test whether, under these comparative conditions, participants would still differentiate between the theft of an insured and an uninsured camera.

Participants. Seventy-nine students (12 male, 67 female) at Tilburg University participated in exchange for course credit (Mage = 19, SD = 3.27).

Design and procedure. Participants were randomly assigned to one of three experimental conditions: separate evaluation—insured victim (SE-I), separate evaluation—uninsured victim (SE-U), or joint evaluation (JE). The same scenario as in the first experiment was used. Hence, the SE conditions constitute replication of Experiment 1. In the JE condition, participants were first asked to read the scenario in which a perpetrator stole an insured camera followed by the scenario in which a different perpetrator stole an uninsured camera. Both scenarios were presented on the same page. Thus, JE participants were implicitly encouraged to compare the two scenarios and were then asked to indicate the appropriate punishment for the described perpetrators. Order of presenting the two scenarios was counterbalanced which evidently did not affect punishment recommendations.

We first compared the punishment recommendations between the two separate evaluation conditions (SE-I and SE-U). Replicating the findings of Experiment 1, an independent t-test revealed that participants recommended less severe punishment for the perpetrator when the victim was insured (M = 9.52; SD = 6.27) than when the victim was uninsured (M = 12.85; SD = 5.39), t (51) = 2.07, p = .04, d = 0.57. For the JE condition, however, a paired sample t-test revealed no significant difference, t (25) = −1.69, p = .10, d = −0.33, indicating that when the two cases were seen together, people punished equally stealing an insured (M = 10.73; SD = 6.37) or uninsured camera (M = 11.19; SD = 6.25). It is noteworthy to point out that only three participants in the JE condition provided different ratings for the two perpetrators. All other participants (89%; 23 out of 26) recommended an identical punishment for the two perpetrators. In sum, when placed in a comparative situation, the majority of participants believe that a punishment should not be a function of the victim’s insurance (or lack of it).1

Experiment 2 demonstrates that the insured victim effect disappears when evaluating both cases jointly. Would people also recommend equal punishments for perpetrators who knowingly stole an insured or uninsured possession respectively? The principle of mens rea (Latin for “guilty mind”) states that “the act does not make a person guilty unless the mind is guilty”. In essence, this principle states that the relevance of a victim’s outcome in sentencing a perpetrator depends critically on the level of foreknowledge when causing harm. For example, involuntary manslaughter refers to the unlawful, but unforeseen, killing of a person while committing a crime (e.g., killing a pedestrian, without intent, when running a red light) and deserves less punishment than murder. In our case, the mens rea principle states that the relevance of insurance in sentencing may depend on whether a perpetrator knew in advance that one’s victim was insured or uninsured. That is, knowingly stealing an uninsured (as opposed to insured) possession is more blameworthy while such a difference is unjustified when the perpetrator was unaware of the victim’s insurance status. In testing the mens rea principle in the domain of insurance and punishment, the next experiment explicitly manipulated whether perpetrators knowingly or unknowingly stole an insured or uninsured possession.

Participants. Eighty-one students (35 male, 46 female; Mage = 21, SD = 2.39) at Fontys University of Applied Sciences participated in exchange for €4. The current study was part of a set of unrelated studies.

Design and procedure. As in the joint evaluation condition in Experiment 2, participants were asked to read the two scenarios concerning the theft of an insured or uninsured camera and subsequently were asked to assess the appropriate punishment each thief deserves. They were randomly assigned to one of two experimental conditions in which they were either informed that both perpetrators knew their victim’s insurance status versus that both perpetrators were unaware of the insurance status of their victims. Order of presenting the two scenarios was counterbalanced; order did not affect punishment recommendations.

We first compared participant’s punishment recommendations for the two perpetrators who unknowingly stole an insured or uninsured camera. A paired sampled t-test revealed no difference in punishing both perpetrators (M = 11.52, SD = 6.17 versus M = 11.50, SD = 6.19), t<1, ns. However, the pattern changed when perpetrators knowingly stole an insured versus uninsured possession. Knowingly stealing an uninsured camera was judged as deserving a harsher punishment (M = 12.18, SD = 5.36) than knowingly stealing an insured camera (M = 11.35, SD = 5.46), t (38) = 2.36, p = .02, d = 0.38. Importantly, while almost no participant (5%; 2 out of 42) recommended different sentences when unknowingly stealing an uninsured or insured possession, significantly more (36%; 14 out of 39) participants imposed different punishments when knowingly stealing an insured or uninsured camera, χ 2 (1,81)= 12.21, p < .001, Cramer’s V = .15.

In sum, people indicate that punishments should not be a function of a victim’s insurance (or lack of it) when perpetrators unknowingly steal insured versus uninsured possessions. A large minority, however, does differentiate between perpetrators who knowingly steal insured versus uninsured possessions. These results confirm that more harm for a victim indeed justifies more punishment, but only when a perpetrator knowingly steals an uninsured versus insured possession. This may suggest that the insured victim effect (see Experiment 1) can be accounted for by participants’ implicit belief that perpetrators were aware of the insurance status of their victim.

In a post experimental test, we therefore asked a different group of participants (N = 15) to read either the insured or uninsured scenario of our first experiment. Subsequently they were asked whether they thought that the perpetrator was aware of stealing an insured or uninsured camera respectively (yes vs. no). A large majority (93%) indicated that they thought the perpetrator was not aware of the (lack of) insurance, ruling out that a difference in foreknowledge drives the insured victim effect.

Although the harm caused to an insured individual is less severe than the harm caused to an uninsured individual, harm is not always a necessary consequence. For example, a perpetrator might be caught in the act leaving the potential victim unharmed. Such an offense still deserves punishment. Would people again differentiate between insured and uninsured individuals when harm was potential but not realized? Insurance may not only change the severity of actual misfortunes, but may also influence thoughts about what could have happened. Research within the domain of counterfactual thinking indeed suggests that, when proposing a sentence for a wrongdoer, people are sensitive for what could have happened to a victim (see Miller & McFarland, 1986; Macrae, 1992). In a similar vein, we propose that being protected from harm by insurance alters what could have happened which in turn evokes the insured victim effect. Experiment 4 addresses this issue by holding constant the outcome of a norm violation (i.e., there is a foul but no harm) while varying only a person’s vulnerability to the consequences if harm had occurred (insured versus uninsured person). In addition, we employed a new vignette in order to determine whether the insured victim effect will replicate using a different norm violation and punishment type. Finally, because we employed a new vignette, we again varied the evaluation mode of participants (separate versus joint evaluation) in order to examine whether we would replicate that the effect (Exeriment 2) disappears when evaluating both cases jointly.

One hundred and nine students (41 male, 67 female, 1 unreported; Mage = 20, SD = 2.68) at Fontys University of Applied Sciences participated in exchange for €4. The current study was part of a set of unrelated studies.

Participants were randomly assigned to one of three experimental conditions: separate evaluation—insured employee (SE-I), separate evaluation—uninsured employee (SE-U), or joint evaluation (JE). Participants in the separate evaluation conditions were asked to read one of the following two scenarios. The scenario in the insurance [no insurance] condition read as follows:

Joris is a student who works for all kinds of companies on a daily basis via an employment agency. He is asked by the agency if he wants to buy disability insurance. This insurance guarantees that Joris, in case of work related injury, will receive specialised rehabilitation that will prevent a lasting disability. Although Joris doubts whether to buy the relatively expensive insurance, he decides [not] to do so. In short, Joris is [not] in the possession of disability insurance.Later that day Joris is employed as a window washer for a company called WASH & GLASS. After receiving a wooden ladder he is instructed to wash numerous windows at three meters height. While climbing up the ladder, it turns out that the fourth step is rotten and Joris falls down and lands on his knee. Joris does not get hurt. Sometime later Joris learns that the owner of WASH & GLASS confessed to the occupational safety authority of being negligent in the maintenance of the ladder. Meanwhile, the owner replaced the ladder. A common punishment for such an offense is to temporarily suspend the company’s working permit. This means that during this period WASH & GLASS is not permitted to work and will lose revenue.

After reading the scenario, participants made their punishment recommendation by indicating the number of days (a minimum of 0 and a maximum of 20 days) the working permit of WASH & GLASS should be suspended. In the JE condition, participants were asked to read an insured and uninsured scenario (applying to different employees and different companies) presented on the same page. Order of presenting the two scenarios was again counterbalanced; order did not affect punishment recommendations.

An unexpected gender difference was observed (male participants punished the business owner less severe than female participants; M =7.05; SD = 5.66 vs. M = 9.91, SD = 5.66), t (107) = 2.55, p = .01, d = 0.50), and in the rest of the analyses we controlled for gender.2 We first compared the punishments imposed by participants in the two separate evaluation conditions (SE-I and SE-U). An analysis of covariance (ANCOVA, including gender as a covariate) revealed that participants recommended a lower punishment when the employee was insured (M = 8.00; SD = 5.50) than when the employee was uninsured (M = 10.37; SD = 5.53), F (1, 72) = 4.35, p = .04, η ² = .05. The pattern in the JE condition was different. For the JE condition, a within-participant ANCOVA revealed that participants did not differentiate when punishing the two business owners. Specifically, participants did not impose a milder punishment for a business owner employing an insured employee (M = 7.70, SD = 6.10) than the owner employing an uninsured employee (M = 7.60, SD = 6.15), F (1, 31) = 1.30, p = .26. Again a large majority (79%; 26 out of 33) of participants in joint evaluation reported an identical punishment recommendation for the two business owners.

This pattern of results is very similar to those obtained in Experiment 2, demonstrating once again the effect of insurance (or lack of it) on punishment recommendations. Although participants believed that the victims’ insurance status should not influence their punishment recommendations (as inferred from the joint-comparative condition), they nevertheless take it into account in their judgment when in a separate, non-comparative condition. Importantly, even in the absence of actual harm, people still recommend less severe punishments for transgressions in which the (potential) victim was insured as opposed to uninsured.

Experiments 2 and 4 demonstrated that the insured victim effect disappears when comparing both cases jointly. Does it imply that people are insensitive to the harm component when comparing both cases in joint evaluation? This would contradict the widespread belief that a punishment should be proportional to the harm caused. Experiment 5 tested the tenet that stealing a possession that is either insured or uninsured can be perceived as more or less harmful depending on how one assesses harm. For example, compare stealing an expensive but insured Mp3 player priced $299 with stealing a relatively inexpensive, uninsured Mp3 player priced $99. In terms of retail prices, the former theft causes more harm than the latter. However, in terms of harm to the victim, the second theft causes more harm because the Mp3 player was not insured. When are people guided by the insurance status of a victim and when by the actual value of the stolen possession in sentencing a perpetrator?

From a legal perspective, the actual value of a stolen possession should outweigh the victim’s insurance status. After all, insurance only transfers the loss from the victim to the insurance company but it surely does not make the total consequences of the crime less severe. However, assessing the value of any object is inherently a comparative judgment and often hard to evaluate in isolation (Hsee, 1996). The purpose of Experiment 5 was to test the proposition that people in joint versus separate evaluation use a legally relevant detail (i.e., the actual value of a stolen possession) differently when punishing a crime in which the value of the stolen possession is hard to evaluate. In order to make the value hard to evaluate, we stated the retail price in a currency of which the value was supposedly unfamiliar to our participants (Japanese Yen). More specifically, participants were asked to impose an appropriate punishment for a perpetrator who either stole an insured camera (priced ¥260.000) or an uninsured camera (priced ¥21.000). Even though the actual price is what people should consider when evaluating how much punishment a perpetrator deserves, this attribute is hard to evaluate. Without a reference, most of our participants would not know whether a camera priced ¥260.000 is expensive or not. In contrast, the insurance status of a victim is relatively easy to evaluate. Most people would evaluate a victim’s harm as little when insured while large when uninsured. It was therefore predicted that people in separate evaluation would punish stealing the insured, expensive camera less harshly while the pattern was expected to reverse in joint evaluation.

A second objective of this experiment was to examine a person’s affective response to the insured victim. Prior research has indicated that less harm is associated with less compassion that in turn is associated with less severe punishment recommendations (e.g., Nadler & Rose, 2003). Given that insurance changes the severity of a victim’s harm, we hypothesized that insured victims evoke less compassion than uninsured victims which, in turn, was predicted to mediate the relationship between a victim’s insurance status and punishment recommendations.

Participants. One-hundred and one students (55 male, 38 female, 8 unreported) at various Dutch universities volunteered to participate (Mage = 22, SD = 4.67, 8 unreported).

Design and procedure. Participants were randomly assigned to one of three experimental conditions: separate evaluation—insured & expensive camera (SE-Iexp), separate evaluation – uninsured & inexpensive camera (SE-Uinexp), or joint evaluation (JE). Participants were asked to read a scenario in which a perpetrator stole a digital camera. The scenario in the insured-expensive camera [uninsured-inexpensive camera] condition read as follows:

Tom decides to buy a digital camera prized ¥260.000 [¥21.000] via the Japanse website of Amazon.com. Amazon also provides the possibility to insure the camera against theft. This type of insurance gurantees that Tom will receive a new camera in case the camera is stolen.Tom decides [not] to buy the insurance. In short, his camera is [not] insured against theft. A few days later when Tom is sitting on the terrace in the city and wants to leave, he discovers that his camera was stolen. Of course, he realizes that he insured [did not insure] the camera.

Some time later Tom finds out that a person is arrested who confessed stealing and selling the camera. A common punishment for such an offence is imposing community service. Community service entails doing compulsory social work for several days (8 hours a day).

In the JE condition, participants were asked to read both the insured-expensive and the uninsured-inexpensive scenario (applying to different victims and perpetrators). Both scenarios were presented on the same page. Order of presenting the two scenarios was counterbalanced and did not affect any of the dependent variables. After reading the scenarios, participants indicated their level of compassion for the victim via the following two questions, (1) how much compassion one felt for the victim (1 = absolutely not, to 7 = absolutely) and (2) how much harm the victim suffered (1 = relatively little, to 7 = relatively much). The items were significantly correlated (r = .41, p < .001) and averaged into a compassion composite. Finally, participants indicated the number of days (a minimum of 1 day and a maximum of 20 days) they thought the perpetrator should fulfill community service. Participants in the two separate evaluation conditions were also asked if they knew the value of 1 Yen in Euros (1= I don’t have any idea to 4 = Yes, exactly; for a similar procedure, see Hsee, 1996). This question was added in order to assess whether participants indeed thought the Japanese currency was hard to evaluate.

Table 1: Experiment 5: Effect of possession type and evaluation mode on compassion for the victim and punishment recommendation.

Insured and expensive Uninsured and inexpensive Separate evaluation Compassion Punishment Joint evaluation Compassion Punishment

Manipulation check. The mean evaluability score for a Japanese Yen was 1.52 (SD = .83) and differed significantly from the midpoint (2.5) of the scale t (65) = − 9.67, p < .001, confirming that the value of the camera was a hard-to-evaluate attribute in this experiment.

Main findings. The main findings are summarized in Table 1. We first compared the two separate evaluation conditions (SE-Iexp and SE-Uinexp). A t-test revealed that insured victims indeed evoked less compassion than uninsured victims. In addition, replicating the insured victim effect, participants recommended a milder punishment for stealing an expensive but insured camera than an inexpensive but uninsured camera. For the JE condition, punishment recommendations reversed. Although the insured victim again evoked less compassion than uninsured victims, participants nevertheless punished stealing the insured but expensive camera more severe than the uninsured, inexpensive camera. These results confirm that people differentiate between a victim’s harm and the actual value of the stolen possession when sentencing perpetrators. When the actual value is hard to evaluate independently, people are guided by the outcome of victims. When the value is evaluated comparatively, however, the value of the possession becomes the primary factor underlying punishment recommendations and the victim’s role is strongly attenuated.

Exploratory mediation analyses. A mediation analysis was applied only to the separate conditions because responses in the joint condition are not independent. We found support for a mediating role of compassion in the insured victim effect, using a series of regression analyses (Baron & Kenny, 1987). Specifically, the relationship of the victim’s insurance status and punishment recommendation (B = 0.26, t = 2.19, p = .032) became non-significant (B = 0.20, t = 1.64, p = .11) when compassion for the victim was added in the analysis (B = 0.22, t = 1.89, p = .07). When evaluating both cases separately, insured victims seem to evoke a less powerful emotional response that, in turn, affects punishment recommendations.

This experiment was designed to explore other potential mediators for the insured victim effect, in addition to the role of compassion. For example, compassion is related to anger and research shows that anger is related to punishment decisions (Kahneman, Schkade, & Sunstein, 1998; Nelissen & Zeelenberg, 2009; Sunstein, 2005). Moreover, transgressions that evoke more compassion are, in general, judged to be more serious or unethical and vice versa. Thus, although Experiment 5 showed that compassion may partly account for our findings, it remains unclear whether the effect is driven solely by compassion or whether it is driven by a change in anger or ethical judgment. In addition, the mediating role of compassion is not sufficient to account for all our findings, because the insured victim effect was observed even in the absence of actual harm (Experiment 4). Given that harm and compassion are intimately related, the absence of harm in Experiment 4 would presumably have resulted in similar degrees of compassion in both experimental conditions. Yet, we still observed the insured victim effect.

The objective of the final experiment was therefore to explore other potential explanations that could account for the insured victim effect namely, a change in anger, ethical judgment or compassion. We employed a new vignette and, as in previous experiments, evaluation mode (separate vs. joint) was manipulated.

Participants. One hundred and thirteen students (14 male, 99 female) at Tilburg University participated in exchange for course credit (Mage = 20, SD = 3.83). The current study was part of a set of unrelated studies. Four participants were discarded for failing a comprehension question.3

Design and procedure. Participants were randomly assigned to one of three experimental conditions: separate evaluation—insured car owner (SE-I), separate evaluation—uninsured car owner (SE-U), or joint evaluation (JE). Participants in the separate evaluation conditions were asked to read one of the following two scenarios. The scenario in the insurance [no insurance] condition read as follows:

Tim recently received his driver’s license. While leaving a parking space he hits another parked car. When stepping out, he notices that his car is undamaged. However, the other car is worse off. The side surface is dented and the paint is damaged. Tim looks around and realizes that no one has seen the accident. Tim doubts what to do. He decides to take off.Sometime later, Tim is arrested. A local resident saw the accident happening from her home. The police report showed that in the meantime the damaged car has already been repaired. The insurance company fully paid for the repair costs. The owner was well insured against such damages [The owner fully paid for the repair costs. The owner was not insured against such damages].

After reading the scenario, we asked a participant the following set of items:

Punishment recommendation. First, a participant indicated a general punishment recommendation by stating how much punishment Tim deserved (1 = mild, to 7 = severe). Next, participants made a specific punishment recommendation by indicating the number of days (a minimum of 1 day and a maximum of 20 days) they thought Tim should fulfill community service.

Compassion. To assess a participant’s compassion for the victim, they were asked (1) how much compassion one felt for the victim (1 = no compassion, to 7 = much compassion) and (2) how much harm the victim suffered (1 = no harm, to 7 = much harm). The items were significantly correlated (r = .53, p < .001) and averaged into a compassion composite.

Ethical judgment of the situation. Participants were told that, “Some offenses are more severe than others. Please indicate the severity of Tim’s offense” (1 = not at all severe, 7 = very severe). In addition, participants were told that, “Some offenses are more unethical than others. Please indicate how unethical Tim’s offense is” (1 = not at all unethical, 7 = very unethical). These items were significantly correlated (r = .51, p < .001) and averaged into an ethical judgment composite.

Feelings of anger. Four items were employed to assess a participant’s anger toward the situation (α = .95). Specifically, participants were asked to indicate how angry the transgression of Tim made them feel; how mad the transgression of Tim made them feel; how angry they were at Tim; and how mad they were at Tim (1= not at all, 7 = very).

Different punishment: Finally, participants in the separate evaluation conditions were asked whether they would punish the perpetrator differently had the victim been uninsured (in the insured victim condition) or insured (in the uninsured victim condition) by indicating: Yes, a more severe punishment; Yes, a less severe punishment; No, the same punishment.

In the JE condition, participants were asked to read an insured and uninsured scenario (applying to different car owners and different perpetrators) presented on the same computer screen.

Table 2: Experiment 6: Effect of victim type and evaluation mode on punishment recommendations, compassion for the victim, ethicality judgments and feelings of anger.

Victim insured Victim uninsured Separate evaluation Punishment general Punishment specific Compassion Ethical Judgment Anger Joint evaluation Punishment general Punishment specific Compassion Ethical judgment Anger

Punishment Recommendations. The main findings are summarized in Table 2. We first compared the two separate evaluation conditions and found that participants recommended milder punishments when the victim was insured. This was true for both the general- and specific punishment recommendation. However, when explicitly asked whether they would change their punishment had the victim been uninsured (in the insured condition) or insured (in the uninsured condition), a large majority of participants (81%; 65/80) indicated that they would not change their sentence. This supports the idea that people believe that insurance should not affect punishments, yet they nonetheless impose milder punishments when victims are insured. This conclusion is even stronger supported by examining the recommendations of participants in the joint condition. When imposing a specific punishment (i.e., community service) for both cases jointly, people again did not differentiate between an insured or uninsured victim. In fact, a large majority (85%; 28/33) imposed identical number of days of community service for both perpetrators, irrespective of the insurance status of their victims. For the general punishment scale, a paired-sample t-test indicated a significant statistical difference when participants compared both cases jointly (i.e., the insured case deserved a less severe punishment than the uninsured case). However, this difference was driven by a small minority of participants. While a large majority (76%; 24/33) provided identical punishment responses for both cases, only 8 out of 33 participants (24%) indicated that both perpetrators should be punished differently.4 Overall, these results confirm that the majority of people believe that a punishment should not be a function of the victim’s insurance, yet people nonetheless impose milder punishments when victims are insured when evaluating both cases separately.

Compassion. Analyzing first the two separate evaluation conditions, the findings of Experiment 5 were replicated showing that insured victims evoked less compassion than uninsured ones. A similar pattern, yet even stronger, was observed in the joint condition. Overall, people seem to feel less compassion for insured victims, irrespective of the evaluation mode of a person.

Ethical Judgment. When comparing the separate evaluation conditions, the results indicate that a victim’s insurance status changes how people evaluate the transgression. Participants judged the act to be less unethical when the victim was insured as opposed to uninsured. A similar pattern emerged when comparing the responses in the joint evaluation condition. A paired-sample t-test revealed that the transgression in the insured case was perceived to be less serious than the uninsured case. However, a large majority of participants in the joint condition (26/33; 79%) provided identical ethicality ratings for both cases, while only 7 out of 33 participants (21%) rated both cases different.5 Overall, these results indicate that the majority of participants seem to believe that the presence of an insured victim should not change the evaluation of the act, yet people nonetheless judge the act to be less severe when evaluating both cases separately. These results support the contention that a victim’s outcome influences the evaluation of the act, even when the outcome is logically irrelevant. Evidently, when evaluating both cases separately, a transgression that resulted in less harm is perceived to be a smaller foul than an identical transgression that happened to result in more harm (see also Gino et al., 2009 for the outcome bias in ethical judgments).

Anger. When comparing the two separate evaluation conditions, we find no evidence for the idea that insured victims arouse less anger than uninsured victims. In joint evaluation however, an insured victim did evoke a less angry response as compared to when the victim was uninsured.

Exploratory mediation analyses. As in Experiment 5, the analysis was applied only in the separate conditions. As initial step, we first inspected the correlations between the potential mediators. Ethical judgments were significantly correlated with compassion for the victim (r = .41, p < .001) and the anger that the situation evoked (r = .54, p < .001) while anger, in turn, was significantly correlated with compassion for the victim (r = .38, p = .001). Overall, these results indicate that the potential mediators are strongly related, yet not fully correlated, suggesting that compassion, anger, and ethical judgment may differentially explain why people become more lenient towards perpetrators when victims are insured.

To examine the mediating role of compassion, anger, and ethical judgment in explaining the insured victim effect, we ran a bootstrap analysis as recommended by Preacher and Hayes (2008) with 5000 bootstrapped samples.6 The results suggest that the insured victim effect was mediated by the change in ethical judgment and not by the change in compassion or anger. Specifically, when we entered compassion, anger, and ethical judgment in the same bootstrapped model simultaneously, the ethical judgment was the only significant mediator, B = 0.27, Z = 2.04, p = .04, with a 95% confidence interval excluding zero (0.0577 to 0.6024). Compassion and anger did not show a significant pattern, compassion B = −0.03, Z = −.35, p = .73; anger B = 0.08, Z = 1.08, p = .28, with both a 95% confidence interval including zero. These results suggest that the presence of an insured victim seems to attenuate the perceived severity of the crime that, in turn, affects punishment recommendations.

In this article we highlight a hidden cost of insurance: People recommend milder punishments for perpetrators when the victim was insured, although people believe that a sentence should not depend on whether the victim was insured or not. The results of six experiments (using a variety of different transgressions and punishments) established the existence of an “insured victim” effect and suggest that people inadvertently differentiate between insured and uninsured victims.

Experiment 1 demonstrated that people would punish identical transgressions less severely when victims are insured as opposed to uninsured. Experiment 2 found that the effect disappeared when participants had to determine jointly the sentence for both the insured and uninsured case. Experiment 3 extended these findings by ruling out that the effect is driven by the perpetrator’s foreknowledge. Experiment 4 demonstrated that when harm was possible but not realized, people still punish crimes less severely when the (potential) victim was insured. Experiment 5 showed that punishment recommendations can even be more lenient for crimes that are in fact more serious but in which the victim was insured. Finally, in Experiment 6, we explored via correlational and mediational analyses, the extent to which a number of potential psychological mechanisms could account for the insured victim effect namely (1) how people evaluate the severity of the transgression, (2) one’s compassion for the victim and (3) the anger that the situation evoked. The results suggest that the insured victim effect is associated with a change in how people evaluate the severity of the transgression and not by a change in compassion or anger.

The present research contributes to a recent stream of research investigating how legally irrelevant characteristics of victims enter judgments of ethical behavior (e.g., Gino et al., 2009; 2010; Cushman et al., 2009; Nordgren & McDonnell, 2011). For example, Nordgren and McDonnell recently showed that increasing the number of people victimized by a crime in turn decreases punishment recommendations (i.e., the more severe the crime in scope, the less punishment). The authors explain their findings by the identifiable victim effect (e.g., Kogut & Ritov, 2005) following which unidentifiable victims evoke less sympathy and less severe punishments than identified victims (Kogut, 2011). We present evidence for a similar effect in which transferring losses to an unidentified entity (i.e., insurance company) results in less severe punishments.

Our work also contributes to a stream of research highlighting the negative intra- and interpersonal consequences of safety mechanisms. For example, Walker (2007) has shown that when overtaking a cyclist, drivers are less cautious (i.e., get closer to the cyclist) when cyclists wear a helmet (analogous to insurance) than when they do not. Thus the safety measure may ironically attract hazard. The present studies supplement this line of research by showing that, other things being equal, insurance may lower the threshold for committing a crime due to possible reduced punishment.

The present results are seemingly incompatible with rationalist theories of moral judgment (Kohlberg, 1969) because of the punishment differences between the separate and joint evaluation modes. These reversals can be elucidated by further examining the important difference between joint and separate evaluation mode (Hsee, 1996; Hsee, Blount, Loewenstein & Bazerman, 1999). Specifically, in the joint mode, which is comparative in nature, it is evident that the severity of the crime is identical (e.g., the same camera was stolen in both cases). The fact that participants in this case impose exactly the same punishment implies that they consider the crime severity as the only relevant dimension (and hence believe that victim’s harm is irrelevant in this case). However, in the separate condition, in which there is no reference point for comparison, the insured victim evoked less compassion and participants evaluated the transgression to be less severe resulting in lower punishment recommendations. In other words, participants’ norm (as inferred from the joint condition) is that compensating a victim’s harm by means of insurance should not have an effect on the size of punishment. Yet, contrary to that belief, and supposedly being unaware of it, participants in the separate condition are swayed by the lack of suffering by the insured victim and, contrary to their standards, inflict a lower punishment in the insured case.

The results reported in the present article were all obtained from a population of laypersons. These findings should therefore be tested on other populations (especially professional judges), although research indicates that professional judges are no different than laypersons in being prone to biases (Vidmar, 2011; Rachlinski, Johnson, Wistrich, & Guthrie, 2009; Landsman & Rakos, 1994). Scenario studies obviously have their limitations, yet we maintain that for revealing punishment recommendations, this method is very useful. Note that legal cases are almost always presented in the form of scenarios to judges and juries.

On a final note, the foregoing results are important not only from a theoretical but also from an applied perspective. Legal systems are often rooted in the premise that punishments should be proportional to the harm caused. However, the harmfulness of an unethical act is evaluated differently when crimes are judged jointly or separately. In separate evaluation, people seem to focus on the consequences of the victims while in joint evaluation people are primarily guided by the harmful consequences of a crime in absolute terms (independent of the consequences to victims). Hence, in separate evaluation, people may be vulnerable to the insured victim effect or other biases. It is important to realize that, in real life situations, judges or jury members are usually in a separate rather than in a joint condition. Legal policy makers should be aware that people in separate evaluation are more easily swayed by legally irrelevant details (such as the insurance status of victims) when sentencing perpetrators. This conclusion is in particular pertinent for jury members who, unlike judges, have no experience and do not reason in a comparative fashion.

Baron, R. M., & Kenny, D. A. (1986). The moderator-mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51, 1173–1182.

Bazerman, M. H., Tenbrunsel, A. E., & Wade-Benzoni, K. A., (1998). Negotiating with yourself and losing: Understanding and managing competing internal preferences. Academy of Management Review, 23, 225–241.

Berg-Cross, L. G. (1975). Intentionality, degree of damage, and moral judgments. Child Development, 46, 970–974.

Carlsmith, K. M., Darley, J. M., & Robinson, P. H. (2002). Why do we punish?: Deterrence and just deserts as motives for punishment. Journal of Personality and Social Psychology, 83, 284 –299.

Cushman, F., Dreber, A., Wang, Y., & Costa J. (2009). Accidental outcomes guide punishment in a “trembling hand” game. PLoS ONE, 4, e6699.

Dave, D., & Kaestner, R. (2009). Health insurance and ex ante moral hazard: Evidence from Medicare. International Journal of Health Care Finance & Economics, 9, 367–390.

Gino, F., Moore, D. A., & Bazerman, M. H. (2009). No harm, no foul: The outcome bias in ethical judgments. Working paper.

Gino, F., Shu, L. L., & Bazerman, M. H. (2010). Nameless + harmless = blameless: When seemingly irrelevant factors influence judgment of (un)ethical behavior. Organizational Behavior and Human Decision Processes, 111, 102–115.

Holmstrom, B. (1979). Moral hazard and observability. The Bell Journal of Economics, 13, 324-340.

Hsee, C. K. (1996). The evaluability hypothesis: An explanation for preference reversals between joint and separate evaluations of alternatives. Organizational Behavior and Human Decision Processes, 67, 247–257.

Hsee, C. K., Blount, S., Loewenstein, G., & Bazerman, M. (1999). Preference reversals between joint and separate evaluations of options: A review of theoretical analysis. Psychological Bulletin, 125, 576–590.

Hsee, C. K., & Kunreuther, H. (2000). The affection effect in insurance decisions. Journal of Risk and Uncertainty, 20, 141 - 160.

Hsee, C. K., & Zhang, J. (2010). General evaluability theory. Perspectives on Psychological Science, 5, 343–355.

Johnson, E. J., Hershey, J., Meszaros, J., & Kunreuther, H. (1993). Framing, probability distortions, and insurance decisions. Journal of Risk and Uncertainty, 7, 35–51.

Kahneman, D., Schkade, D., & Sunstein, C. R. (1998). Shared outrage and erratic awards: The psychology of punitive damages. Journal of Risk and Uncertainty, 16, 49–86.

Kogut, T. (2011). The role of perspective-taking and emotions in punishing identified and unidentified wrongdoers. Cognition and Emotion, 25, 1491–1499.

Kogut, T., & Ritov, I. (2005). The identifiable victim effect: An identified group, or just a single individual. Journal of Behavioral Decision Making, 18, 157–167.

Kohlberg, L. (1996). Stage and sequence: The cognitive-developmental approach to socialization. In D.A. Goslin (Ed.), Handbook of socialization theory and research (pp. 347-480). Chicago: Rand McNally.

Landsman, S. & Rakos, R. F. (1994). A preliminary inquiry into the effect of potentially biasing information on judges and jurors in civil litigation. Behavioral Sciences and the Law, 12, 113–126.

Macrae, C. N. (1992). A tale of two curries: Counterfactual thinking and accident-related judgments. Personality and Social Psychology Bulletin, 18, 84–87.

McCaffery E. J., Kahneman, D., & Spitzer, M. L. (1995). Framing the jury: Cognitive perspectives on pain and suffering awards. Virginia Law Review, 81, 1341–1420.

Miller, D. T, & McFarland, C. (1986). Counterfactual thinking and victim compensation: A test of norm theory. Personality and Social Psychology Bulletin, 12, 513–519.

Nadler, J., & Rose, M. R. (2003). Victim impact testimony and the psychology of punishment. Cornell Law Review, 88, 419–456.

Nelissen, R. M. A., & Zeelenberg, M. (2009). Moral emotions as determinants of third-party punishment: Anger, guilt, and the functions of altruistic sanctions. Judgment and Decision Making, 4, 543–553.

Nordgren, L. F., & McDonnell, M. H. (2010). The scope-severity paradox: Why doing more harm is judged to be less harmful. Social Psychological and Personality Science, 2, 97–102.

Paharia, N., Kassam, K. S., Greene, J. D., & Bazerman, M. H. (2009). Dirty work, clean hands: The moral psychology of indirect agency. Organizational Behavior and Human Decision Processes, 109, 134–141.

Preacher, K. J., & Hayes, A. F. (2008). Asymptotic and resampling strategies for assessing and comparing indirect effects in multiple mediator models. Behavior Research Methods, 40, 879–891.

Rachlinski, J., Johnson, S., Wistrich, A., & Guthrie, C. (2009). Does unconscious racial bias affect trail judges? Notre Dame Law Review, 84, 1195–1246.

Stanciole, A. E. (2007). Health insurance and life style choices: Identifying the ex ante moral hazard. IRISS Working Paper Series.

Sunstein, C. R. (2005). Moral heuristics. Behavioral and Brain Sciences, 28, 531–573.

Tykocinski, O. E. (2008). Insurance, risk, and magical thinking. Personality and Social Psychology Bulletin, 34, 1346–1356.

Van Wolferen, J., Inbar, Y., & Zeelenberg, M. (2013). Magical thinking in predictions of negative events: Evidence for tempting fate but not for a protection effect. Judgment and Decision Making, 8, 45–54.

Vidmar, N. (2011). The psychology of trail judging. Current Directions in Psychological Science, 20, 58–62.

Walker, I. (2007). Drivers overtaking bicyclists: Objective data on the effects of riding position, helmet use, vehicle type, and apparent gender. Accident Analysis and Prevention, 39, 417–425.

This research is supported by funding provided by Netspar, Network for Studies on Pensions, Aging, and Retirement. We thank Marcel van Assen for help on statistics in Experiment 6.

Copyright © 2013. The authors license this article under the terms of the Creative Commons Attribution 3.0 License.

This document was translated from LATEX by HEVEA.