Judgment and Decision

Making, vol. 1, no. 2, November 2006, pp. 153-158.

The rich get richer and the poor get poorer:

On risk aversion in behavioral decision-making

Ingmar H. A. Franken1, Irina Georgieva, Peter Muris

Institute of Psychology, Erasmus University Rotterdam, The

Netherlands,

Ap Dijksterhuis

Department of Psychology

University of Amsterdam

Abstract

Some studies have found that choices become more risk averse

after gains and more risk seeking after losses, although other

studies have found the opposite. The latter tend to use

hypothetical cases that encourage deliberation. In the current

study, we examined the effects of prior gains and losses on a

task designed to encourage less reflective decision making, the

Iowa Gambling Task (IGT). Fifty participants conducted a

manipulated decision-making task in which one group gained

money, whereas the other group lost money, followed by the IGT.

Participants who experienced a prior monetary loss displayed

more risky choice behavior on the IGT than subjects who

experienced a prior gain. These effects were not mediated by a

positive or negative affect, although the sample size may have

been too small to detect a small effect.

Keywords: implicit decision-making, reward, punishment,

Iowa Gambling Task, monetary choices, risk behavior.

1 Introduction

Kahneman and Tversky (1979) noted that people are often risk

averse for gains and risk seeking for losses. Whether people

consider a consequence of their choice as a loss or as a gain is

dependent on their point of reference. This reference point,

which is often equivalent to the current wealth position, plays a

key role in the theory of choice.

It should be possible to manipulate perceptions of the domain

(gain or loss) with actual prior gains or losses. People may see

their starting point, before the gain or loss, as the reference

point. If they had lost money, for example, they may see new

gambles as in the domain of losses, and they therefore might be

risk seeking. Earlier studies of the effect of gains and losses

show conflicting results. Thaler and Johnson (1990) found the

opposite results - which they called a "house money effect"

- although their participants would take risks to gain back all

of their loss. Weber and Zuchel (2005) review this literature

and find some conditions that support the Prospect Theory

prediction. Aside from their result, however, most of the

results consistent with Prospect Theory are from studies that use

more realistic situations such as investment, rather than

hypothetical tasks.

Some traditional economic studies addressing theories of

decision-making assume that decision-making is based on deliberate

evaluations of varying option-outcome scenarios, that is, people weigh

the pros and cons of various choices against each other and base their

decision on the outcome of this comparison. These kinds of choices can

be characterized as deliberate, and carefully thought-out.

However, some recent psychological studies addressing decision-making

show that decisions can also be driven by less carefully thought-out

choices (Dijksterhuis, Bos, Nordgren, & van Baaren, 2006), are often

implicit and automatic (Hastie, 2001), and are based on

"gut-feelings" (Damasio, 1996) or emotions

(Loewenstein et al., 2001; Sanfey, Loewenstein, McClure, & Cohen,

2006). Recently, Sanfey et al. (2006) made a clear distinction between

these two psychological systems involved in economic decision-making:

an emotional system, which involves the activation of automatic

processes and a deliberative system involving controlled processes,

with each having separate neural substrates. In the present

contribution, we want to apply this recent knowledge to risk aversion.

Is risk aversion after gains the consequence of people's

deliberate, conscious decisions to avoid risk? Or is the case that risk

aversion can largely automatic, whereby people's

current reference point leads them to pursue less risky options without

deliberately weighting all outcome scenarios?

In the present study we examined the role of reference point in a

task designed to encourage automatic, emotional driven

decision-making, the Iowa Gambling Task (IGT). During the IGT

participants have to select cards from four decks that range in

probability and magnitude of rewards and punishments (Bechara,

Damasio, Damasio, & Anderson, 1994; Bechara, Damasio, &

Damasio, 2000). To translate our hypothesis pertaining to risk

aversion to the IGT, it is necessary to explain the IGT in some

detail. In the IGT, participants can repeatedly choose (usually

up to 100 times) between four decks of cards. Two of the

decks (e.g., A and B) are disadvantageous. They produce large

immediate gains, but these gains are followed by large losses,

leading to an overall loss in the long run. The other remaining

decks (e.g., C and D) are advantageous. The gains are modest but

consistent and the losses are small. Consistently choosing these

decks leads to gains in the long run. This means that people who

are risk seeking would be predominantly choose decks A and B,

leading to losses in the long run. Conversely, people who are

risk averse will predominantly choose decks C and D, leading to

overall gain. This means that risk aversion translates into

better performance (overall gains) on the IGT, whereas risk

seeking would translate into poor performance (overall losses).

The psychological process that determines people's

behavior in the IGT is crucial to our hypothesis that risk aversion is

not only based on deliberately weighting all outcome scenarios. A

general consensus is that people performing the IGT at some point steer

towards certain (profitable) decks, in rather automatic way. Whether

this automatic behavior is entirely unconscious is still subject to

debate; see Maia and McClelland (2004), and Dunn et al. (2006).

Behavior on the IGT can be seen as a form of implicit learning (Reber,

1993), whereby behavior changes before people can verbalize why they do

what they are doing. Therefore, the IGT can be regarded as an

instrument capable of assessing intuitive and emotion-based

decision-making processes.

In addition to our central aim - to test the relative automaticity of

risk aversion - we have another goal. Economic studies addressing

theories of decision-making often rely on hypothetical situations and

choices in which participants are confronted with monetary gambles

without any real consequences. Although the use of real incentives is

often not crucial for the outcome of experiments, using real incentives

has an important role to play in establishing the quality, credibility,

and generalizability of experimental data (Beattie and Loomes, 1997).

In the present study, we addressed this point by using real monetary

remunerations in order to mimic real-life decision-making more closely.

For the purpose of the present study, we experimentally manipulated the

reference point. That is, participants first performed a manipulated

gamble-task in which they either gained or lost money as a result of

their performance (in actuality, they had no influence on these gains

or losses). Note that this experimental set-up comes close to real-life

situations in which a person's reference point (real

or perceived) is often the result of their prior choices.

It is known that individual differences can influence behavioral

decision-making. These individual difference variables include reward

sensitivity (Franken & Muris, 2005), gender (Overman, 2004), and age

(Wood, Cox, Davis, Busemeyer, & Koling, 2005). In line with previous

research (Peters & Slovic, 2000), we expected that our experimental

manipulation would have an effect on participants'

affect. More precisely, a prior gain would yield an increase of

positive affect, whereas an earlier loss would result in an increase of

negative affect. It has been suggested that affect might influence

decision-making (Ashby, Isen, & Turken, 1999; Loewenstein et al.,

2001). Positive affect can promote increased sensitivity to losses

(Isen, Nygren, & Ashby, 1988). In the present study, we investigated

whether the above-mentioned individual differences and affect may have

an additional effect on the participants'

decision-making.

The main hypothesis was that people who experienced a prior gain on a

gambling task performed better (i.e., made more advantageous choices as

a consequence of risk aversion) on the IGT as compared to persons who

experienced a prior loss. Furthermore, we asked whether this

effect was influenced by subjective affect, and various other

individual differences.

2 Method

2.1 Participants

Fifty undergraduate psychology students (11 males) were recruited

to participate in the present study. Their mean age was 20.6

years (SD = 3.2). All participants received course credits for

participating and could gain additional money depending on their

performance on the IGT, ranging between 1 and 6 .

Participants were randomized into two groups: a Prior Loss (PL)

group (n = 25; 5 males) or a Prior Gain (PG) group (n = 25; 6

males). All subjects signed informed consent prior to the

beginning of the experiment.

2.2 Instruments

For the present study we used the computerized version of the IGT

to measure decision-making (Bechara, Tranel, & Damasio, 2000; we

used the same monetary outcomes but substituted Euros for

dollars). This task consists of 100 successive trials, which were

split into five 20-trial blocks for analysis, in which subjects

are instructed to try to gain as much money as possible by

drawing cards from one of four decks. The decisions to choose

from the decks are motivated by reward and punishment schedules

inherent in the task. Two of the decks (i.e., A and B) are

disadvantageous, producing immediate gains (large rewards) but

these are accompanied by larger losses in the long run (larger

punishments). The C and D decks are advantageous: gains are

modest but more consistent and losses are smaller. See Bechara,

Tranel, & Damasio, 2000, for the payoff and probability scheme

of the IGT. The net-score (the number of advantageous decks

choices minus the number of disadvantageous decks choices) was

used as dependent variable. A higher score indicates that a

subject is more often choosing advantageous decks. There is

general consensus that the "IGT has proved to be a sensitive,

ecologically valid measure of decision-making" (Dunn et al.,

2006).

The BIS/BAS Scales (Carver & White, 1994) were presented as a

self-report questionnaire that has been constructed to assess

individual differences in personality dimensions that reflect the

sensitivity of two motivational systems, the aversive and appetitive

system (BIS and BAS; Gray, 1987). The BIS/BAS Scales consist of 20

items that can be allocated to two primary scales: the Behavioral

Inhibition System scale (BIS; 7 items) and the Behavioral Approach

System scale (BAS; 13 items). The BAS can be divided into 3 subscales:

Fun Seeking (4 items), Reward Responsiveness (5 items), and Drive (4

items). The Dutch version of the BIS/BAS Scales has been described in

previous studies (Franken, 2002; Franken, Muris, & Rassin, 2005).

Cronbach's alphas for various scales were found to

range from .61 to .79.

The Positive and Negative Affect Scales (PANAS; Watson, Clark, &

Tellegen, 1988) were administered as a measure of positive and

negative affect. The PANAS is a 20-item bidimensional mood

inventory with a 5-point Likert-scale response format. Positive

affect reflects the extent to which a person feels enthusiastic,

active, and alert, whereas negative affect is a general dimension

of subjective distress and unpleasurable engagement that subsumes

a variety of aversive mood states, including anger, contempt,

disgust, guilt, fear, and nervousness (Watson et al., 1988).

Psychometric properties of the PANAS scales are good (Boon &

Peeters, 1999; Watson et al., 1988).

2.3 Procedure and manipulation

Participants were told that they participated in a gambling study

and that we aimed to investigate decision-making qualities.

First, participants completed all questionnaires. Subsequently,

half of the subjects carried out the "loss" version of the

manipulated IGT, while the other half conducted the "gain"

version of the manipulated IGT. For both groups, we used a

fixed, pseudo-random, gain/loss schedule irrespective of the

choices that participants made. This manipulated IGT was

programmed to yield a gain of four in the PG group and a

loss of 10 in the PL group. Irrespective of the card

choice, there was always a pre-determined pattern of

gains/losses. The proportion of cards with losses were in all

tasks and all decks 50%. There were no differences among the A,

B, C, and D decks, they were all equal. The difference between

the PL and PG condition was were the amount of losses, which were

of course larger in the PL condition. In order to make the

reference point (i.e., gain or loss) more salient (Heath,

Larrick, & Wu, 1999), participants in the PG group were told

that they gained money above average on this task, whereas

participants in the PL group were told that they lost more than

average on this task. In addition, participants were instructed

that complete new rules applied to the second game, that they

needed to employ other decision-strategies in order to gain

money, and that other decks would be advantage and disadvantage.

Again, they were told that some decks would be more advantageous

than others. Furthermore, all participants were told that their

prior loss or gain would be the starting point for the second

task. In other words, the PG group started with an initial credit

of four , and the PL group started with an initial debt of 10

. After the manipulated IGT, subjects completed the PANAS for

a second time in order to measure whether the experimental

manipulation resulted in a change of affect. Finally,

participants carried out the "real" IGT, which measured their

actual behavioral decision-making.

2.4 Analysis

In order to test the main hypothesis, an hierarchical regression

analysis was carried out with the IGT net-score as dependent

variable and age, gender, group, affect (pre minus post affect

scores2), and BIS, and BAS as covariates. We entered gender

and age in the first block of the regression, group in the

second, positive and negative affect in the third, and BIS and

BAS in the fourth block. Additionally, differences on affect (pre

versus post) were tested using a 2 (time) x 2 (group) ANOVA.

Further, in order to investigate the performance of the two

groups per block (i.e., 20 cards), a multivariate ANOVA (MANOVA)

was performed with the scores on the five subsequent blocks as

dependent variables.

2.5 Results

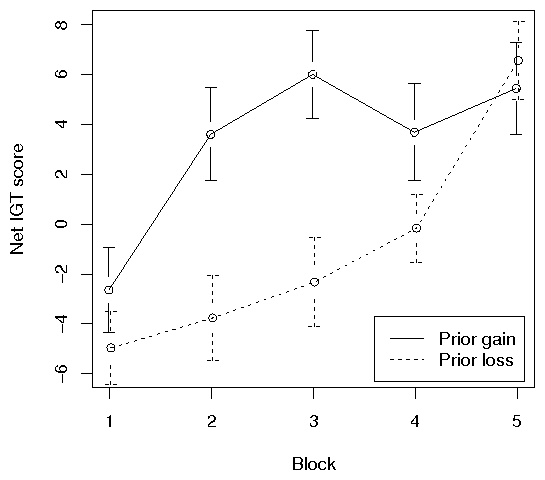

Figure 1: IGT score over the five blocks per group (with standard

errors).

Figure 1 displays the mean IGT net scores of both groups over the

five blocks. As can be seen in Table 1, the group variable made a

unique and significant contribution to IGT-scores. Age, gender,

affect, BIS, and BAS did not predict IGT-scores, indicating that

these variables, including affect, had no influence on decision

making.

Table 1: Results of hierarchical regression analyses predicting

performance on the net score of the Iowa Gambling Task.

Figure 1: IGT score over the five blocks per group (with standard

errors).

Figure 1 displays the mean IGT net scores of both groups over the

five blocks. As can be seen in Table 1, the group variable made a

unique and significant contribution to IGT-scores. Age, gender,

affect, BIS, and BAS did not predict IGT-scores, indicating that

these variables, including affect, had no influence on decision

making.

Table 1: Results of hierarchical regression analyses predicting

performance on the net score of the Iowa Gambling Task.

| B

| S.E. B

| b

| D2 R

|

|

Step 1

| | | | .01

|

| Gender

| 0.49

| 1.27

| -0.06

| |

| Age

| -2.94

| 9.54

| -0.05

| |

|

Step 2

| | | | .15*

|

| Group

| -21.32

| 7.35

| -0.40*

| |

|

Step 3

| | | | .00

|

| Positive Affect

| -0.17

| 0.62

| -0.04

| |

| Negative Affect

| 0.24

| 0.70

| 0.06

| |

|

Step 4

| | | | .02

|

| BIS

| -1.19

| 1.25

| -0.15

| |

| BAS

| -0.18

| 0.85

| -0.03

| |

|

|

| * p .001. |

There was a significant group x time effect for positive affect,

F(1,48) = 10.32, p = .002, and negative affect F(1,48) = 31.54, p

= .000001. More specifically, the manipulated IGT resulted in an

increase in positive affect in the PG group and an increase in

negative affect in the PL group. However, in the regression

analysis, this change in affect did not influence the relation

between the prior loss or gain and "real" IGT performance.

The MANOVA showed a significant multivariate effect, Wilks'

lambda = .75, F(5,44) = 2.89, p = .024. Follow-up MANOVAs

performed on the participants performance on the separate blocks

revealed a significant difference in the IGT scores for block 2,

F(1,42) = 8.41, p = .006, and block 3, F(1,42) = 11.05, p = .002.

The fact that only in blocks 2 and 3 participants in the PG group

made more advantageous choices than participants in the PL group

is consistent with our theorizing. In block 1, people are

generally oblivious to the nature of the decks, leading to rather

random choice behavior. In blocks 2 and 3, people are developing

preferences for certain decks, leading to more systematic

choices. Later during the task (blocks 4 and up), more and more

people start to understand the nature of the decks, leading to

consistent favorable (risk averse) choices irrespective of

experimental condition.

3 Discussion

Our results show that a reference point manipulation using prior

gains or losses affected decisions with monetary consequences.

The study adds further experimental evidence that people who

"have" make more risk-averse decisions, while the "have-nots"

make more risk-seeking decisions. This phenomenon has frequently

been observed from studies using hypothetical decision-making

situations (Thaler & Johnson, 1990) and agrees with the

increased risk aversion principle of Prospect Theory. This

theory predicts exactly what we found, that is, prior losses put

the subject in the domain of losses and prior gains have the

opposite effect.

Insofar as the IGT is, as hypothesized, sensitive to

non-deliberative mechanisms of decision making, our results show

that risk seeking and risk aversion as a function of prior gains

and losses does not need to be the result of a deliberate,

well-considered choice strategy: risk seeking and risk aversion

can be automatic and non-deliberately, it can be seen as a

spontaneous process, steering people towards or away from risk.

A secondary goal was to investigate the role of emotions

(affect). We successfully induced positive affect in the PG group

and negative affect in the PL group. However, affect variables

did not influence the relation between prior loss/gain and

decision-making. Additional correlation analysis between

positive/negative affect scores (i.e., pre, post, and pre-post

difference scores) and IGT score showed that there were no

significant links between affect and decision-making (all p's

.05). Accordingly, from the present findings, it

can be concluded that the effect of a reference point on

behavioral decision was not mediated by positive or negative

affect. This is in contrast with earlier findings of Peters and

Slovic (2000), who found that high negative affect was associated

with more avoidance of high-loss options and high positive affect

was associated with more choices from high-gain options. An

explanation for these different results might be that Peters and

Slovic used a different version of the Iowa gambling task.

Whereas we used the original task, Peters and Slovic used a

gambling task that was on several points different from the

original task. In addition, the present sample size may have

insufficient power to detect a significant result concerning the

influence of affect.

Although it is conceivable that, by the fifth block, PL

participants might have thought that the risky decks could undo

their prior loss, this could not occur in the second block, and

the difference between PL and PG conditions was already present.

Thus, we conclude that the PL does increase risk seeking in the

IGT, as predicted by Prospect Theory.

References

Ashby, F. G., Isen, A. M., & Turken, U. (1999). A neuropsychological

theory of positive affect and its influence on cognition.

Psychological Review, 106, 529-550.

Beattie, J., & Loomes, G. (1997). The impact of incentives upon risky

choice experiments. Journal of Risk and Uncertainty, 14(2),

155-168.

Bechara, A., Damasio, A. R., Damasio, H., & Anderson, S. W. (1994).

Insensitivity to future consequences following damage to human

prefrontal cortex. Cognition, 50, 7-15.

Bechara, A., Damasio, H., & Damasio, A. R. (2000). Emotion, decision

making and the orbitofrontal cortex. Cerebral Cortex, 10,

295-307.

Bechara, A., Damasio, H., Tranel, D., & Damasio, A. R. (1997). Deciding

advantageously before knowing the advantageous strategy.

Science, 275, 1293-1295.

Bechara, A., Tranel, D., & Damasio, H. (2000). Characterization of the

decision-making deficit of patients with ventromedial prefrontal cortex

lesions. Brain, 123, 2189-2202.

Boon, M. T., & Peeters, F. P. (1999). Affectieve dimensies bij

depressie en angst (Dimensions of affectivity in depression and

anxiety). Tijdschrift voor Psychiatrie, 41, 109-113.

Carver, C. S., & White, T. L. (1994). Behavioral inhibition, behavioral

activation, and affective responses to impending reward and punishment:

The BIS/BAS scales. Journal of Personality and Social

Psychology, 67, 319-333.

Crone, E. A., Bunge, S. A., Latenstein, H., & Van Der Molen, M. W.

(2005). Characterization of children's decision

making: Sensitivity to punishment frequency, not task complexity.

Child Neuropsychology, 11, 245-263.

Damasio, A. R. (1996). The somatic marker hypothesis and the possible

functions of the prefrontal cortex. Philosophical Transactions

Of The Royal Society Of London. Series: B-Biological Sciences, 351,

1413-1420.

Dijksterhuis, A., Bos, M. W., Nordgren, L. F., & van Baaren, R. B.

(2006). On making the right choice: the deliberation-without-attention

effect. Science, 311, 1005-1007.

Dunn, B. D., Dalgleish, T., & Lawrence, A. D. (2006). The somatic

marker hypothesis: A critical evaluation. Neuroscience and

Biobehavioral Reviews, 30, 239-271.

Franken, I. H. A. (2002). Behavioral approach system (BAS) sensitivity

predicts alcohol craving. Personality and Individual

Differences, 32, 349-355.

Franken, I. H. A., & Muris, P. (2005). Individual differences in

decision-making. Personality and Individual Differences, 39,

991-998.

Franken, I. H. A., Muris, P., & Rassin, E. (2005). Psychometric

properties of the Dutch BIS/BAS Scales. Journal of

Psychopathology and Behavioral Assessment, 27, 25-30.

Gray, J. A. (1987). The psychology of fear and stress.

Cambridge: Cambridge University Press.

Hastie, R. (2001). Problems for judgment and decision making.

Annual Review of Psychology, 52, 653-683.

Heath, C., Larrick, R. P., & Wu, G. (1999). Goals as reference points.

Cognitive Psychology, 38, 79-109.

Hertwig, R., & Ortmann, A. (2001). Experimental practices in economics:

a methodological challenge for psychologists? Behavioral and

Brain Sciences, 24, 383-403.

Huber, O., Wider, R., & Huber, O. W. (1997). Active information search

and complete information presentation in naturalistic risky decision

tasks. Acta Psychologica, 95, 15-29.

Isen, A. M., Nygren, T. E., & Ashby, F. G. (1988). Influence of

positive affect on the subjective utility of gains and losses: it is

just not worth the risk. Journal of Personality and Social

Psychology, 55, 710-717.

Kahneman, D., & Tversky, A. (1979). Prospect Theory: An analysis of

decision under risk. Econometrica, 47, 263-292.

Loewenstein, G. F., Weber, E. U., Hsee, C. K., & Welch, N. (2001). Risk

as feelings. Psychological Bulletin, 127, 267-286.

Maia, T. V., & McClelland, J. L. (2004). A reexamination of the

evidence for the somatic marker hypothesis: What participants really

know in the Iowa gambling task. Proceedings of the National

Academy of Sciences of the United States of America, 101, 16075-16080.

Overman, W. H. (2004). Sex differences in early childhood, adolescence,

and adulthood on cognitive tasks that rely on orbital prefrontal

cortex. Brain and Cognition, 55, 134-147.

Peters, E., & Slovic, P. (2000). The springs of action: Affective and

analytical information processing in choice. Personality and

Social Psychology Bulletin, 26, 1465-1475.

Reber, A. S. (1993). Implicit learning and tacit knowledge: An

essay on the cognitive unconscious. New York: Oxford University Press.

Sanfey, A. G., Loewenstein, G., McClure, S. M., & Cohen, J. D. (2006).

Neuroeconomics: cross-currents in research on decision-making.

Trends in Cognitive Science, 10, 108-116.

Thaler, R. H., & Johnson, E. J. (1990). Gambling with the house money

and trying to break even: The effects

of prior outcomes on risky

choice. Management Science, 36(6), 643-660.

Watson, D., Clark, L. A., & Tellegen, A. (1988). Development and

validation of brief measures of positive and negative affect: The PANAS

Scales. Journal of Personality and Social Psychology, 54,

1063-1070.

Weber, M. & Zuchel, H. (2005). How do prior outcomes affect

risk attitude? Comparing escalation of commitment and the

house-money effect. Decision Analysis, 2, 30-43.

Wood, S., Cox, C. R., Davis, H., Busemeyer, J., & Koling, A. (2005).

Older adults as adaptive decision makers: Evidence from the Iowa

Gambling Task. Psychology and Aging, 20, 220-225.

Footnotes:

1This work was supported by

the Netherlands Organization for Scientific Research (NWO).

Ingmar Franken, Institute of Psychology, Erasmus University

Rotterdam, Woudestein J5-43, P.O. Box 1738, 3000 DR

Rotterdam, The Netherlands, E-mail:

franken@fsw.eur.nl

2Using pre-manipulated IGT and post-manipulated

IGT affect scores in the regression model yielded similar

results.

File translated from

TEX

by

TTH,

version 3.74.

On 16 Nov 2006, 10:38.